A report by the “World Inequality Lab” showed that inequality in India is at a historic high, even when compared to British rule. The study reveals a stark reality: income inequality in India has reached unprecedented levels, outpacing even nations like the U.S., Brazil, and South Africa. The country now has 271 billionaires, with 94 new additions in 2023 alone, according to the Hurun Research Institute. This surge in wealth, concentrated among a small elite, represents nearly $1 trillion—7% of global wealth. Economists, including Thomas Piketty, note that this “Billionaire Raj” has created disparities so vast that by some measures, income distribution in colonial India was more equitable than it is today.

While India is celebrated for its rapid economic growth—projected to become the world’s third-largest economy by 2027—these figures mask the economic struggles of its broader population. The unemployment rate for young adults aged 20 to 25 stands at an alarming 40%, with 60-65% of the unemployed being educated, according to the International Labour Organization.

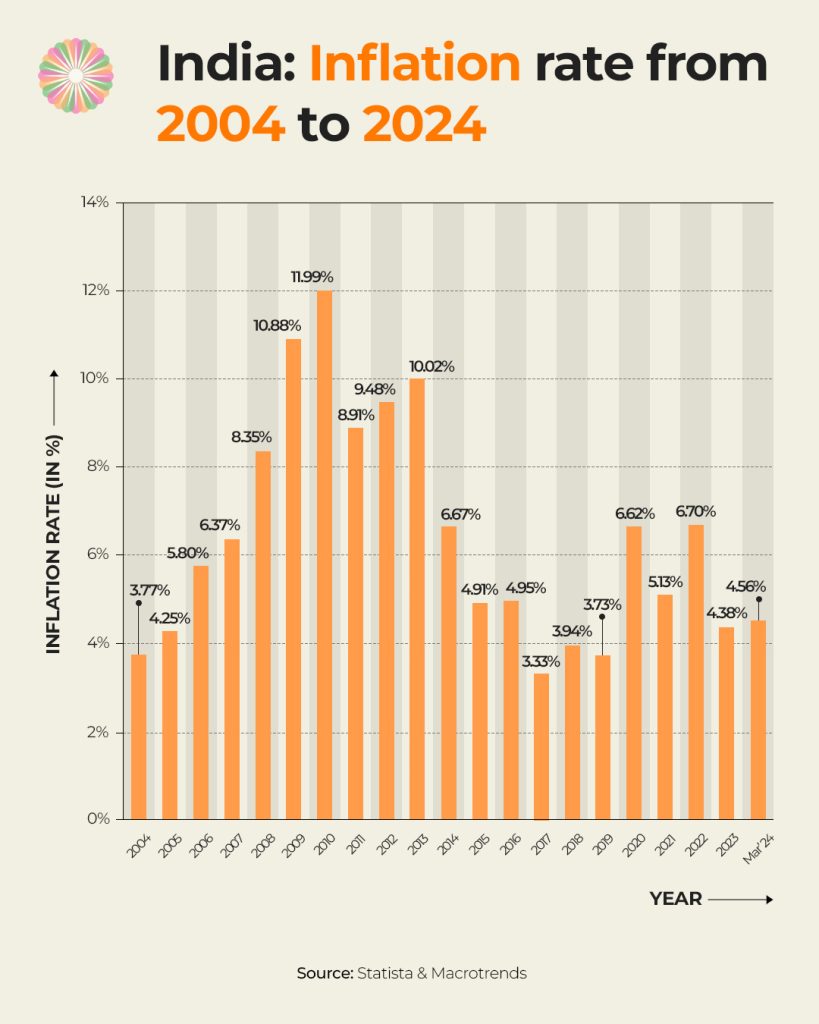

Inflation of essential commodities, such as vegetables (27%), pulses (19.5%), and cereals (7.8%), adds further strain to households. Coupled with a national debt of ₹160 lakh crore and household savings at just 5%, the gap between India’s wealthy elite and the struggling majority continues to widen.

The World Inequality Lab’s study underscores the urgent need for policy interventions to address these disparities. Despite being hailed as an emerging global economic powerhouse, India must tackle its deepening inequality to ensure that growth translates into tangible benefits for all. Without measures to curb unemployment, reduce inflation, and foster more equitable wealth distribution, the economic achievements of the few will remain overshadowed by the struggles of the many.

Are You Passionate About India's Future? Join Our Community to Collaborate, Advocate, and Create Positive Change.